How exactly do you imagine your QuickBooks experience? Smooth and productive, right? But this whole experience is interrupted by random errors, which no one is prepared for. When you come across an error in QuickBooks that isn’t just an error, it brings down the software functionalities, risks your crucial data and what not. And so, these errors need to be taken down immediately, especially when it comes to errors like the "QuickBooks error 6138 1005". This error generally occurs when a user try to open or access a company file in QuickBooks but it failed to open due to damaged company files, incorrect hosting configuration or network-related issues. When this error appears, QuickBooks may fail to open the company file properly and users may temporarily lose access to important accounting data. This segment is going to be all about the this error, its causes, fixes, and much more.

We understand the struggle of tackling through the random errors that usually pop up when trying to access the company file locally or over a network, just like this one, and so our team has curated this guide touching upon the sensitive yet helpful information about such errors in QuickBooks.

What is QuickBooks error code 6138, -1005?

QuickBooks error code 6138 1005 is basically a technical glitch that falls under the category of 6xxx series. It is one of the most common error in QuickBooks accounting software. These errors are company file related issue and usually occurs when QuickBooks desktop cannot access or communicate with the company file properly. These errors are commonly seen in multi-user environments where multiple workstations are try to attempt to access the same company file that is stored on a server. The fixation of such issues are much similar, but as they are associated with the company file, they need to be taken care of well. As you experience the issue at the time of accessing company file, it gives us a hint that the company file might be hosted by a system other than the server.

What are the factors triggering to QuickBooks error 6138 1005?

While the possible triggers can be many, but here we have tried to cover the most common ones to help you understand the issue better:

Your folders might show signs of corruption ultimately causing such issues.

If your .nd and .tlg files are showing signs of damage.

In case of long company file path exceeding character limits, this can also lead to this error.

If you haven’t followed the correct procedure to install QuickBooks desktop and it turned out to be a failure, then such errors are quite possible to show up.

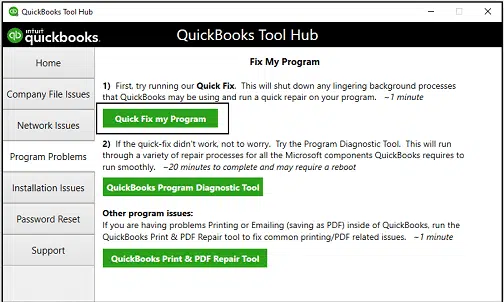

Once the installation completes, launch the Tool Hub.

After that head to Program Problems tab.

Select Quick Fix My Program option and let the tool run properly.

This process might take a couple of minutes depending upon your system performance.

Once the tool finishes the repair process, reopen QuickBooks desktop and check whether the issue gets fixed successfully or not.

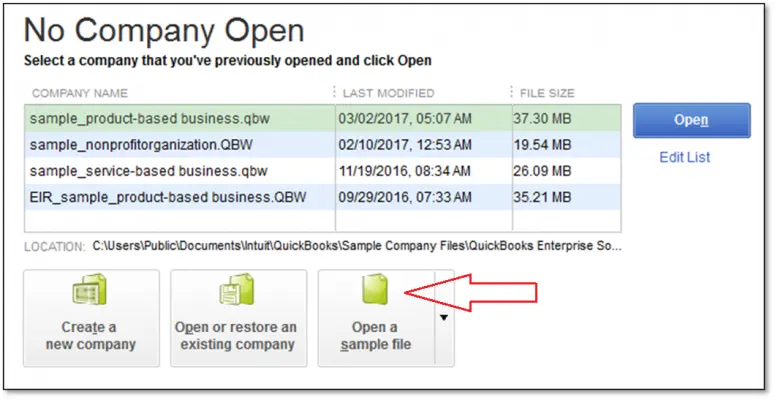

Solution 4: Try to run a sample company file

Under this procedure, double click the QuickBooks accounting software.

Followed by proceeding to the No company open window and there pick the Open a Sample file tab.

Opt for the File from the list of sample company files.

If you still come across the same error message, then you definitely require to repair your software installation.

Whereas, if the file opens smoothly, then you probably are facing issues with the company file, which can be resolved using a bunch of other methods.

Solution 5: Getting QuickBooks company file backup restored

Your current company file might face issues, in case you have made any recent changes that aren’t working according to the plan, and so you can get access to your company file backup, as it might help you to get a company file without any error.

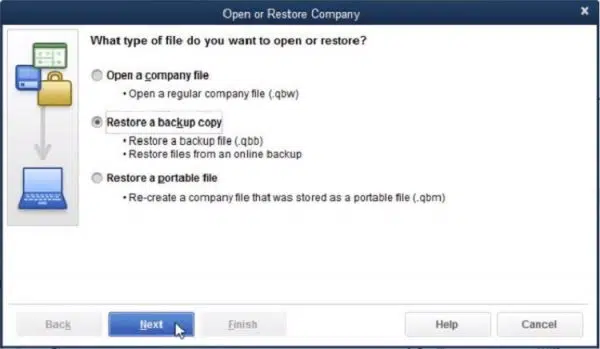

Start the process by moving to the QuickBooks File menu.

Then go to the Open or restore company option.

You would also have to tap on to Restore a backup copy option.

Now tap on Next and find the Local backup option.

Pick the Next tab.

Later on search for the system to identify the backup version of the company file.

The last step is to pick a folder that you wish to save the file you just restored.

Solution 6: Turn off the hosting

This process is something that you can opt for the file over a network. In such case, you are supposed to simply turn off the hosting using the process shared below:

Simply press the F2 key to open the Product Information window.

After that, head to the Local Server Information section.

Then check the hosting status carefully to verify whether hosting is turned on or not.

If hosting is enabled on the workstation, then make sure to turn it OFF immediately. To do, follow these steps:

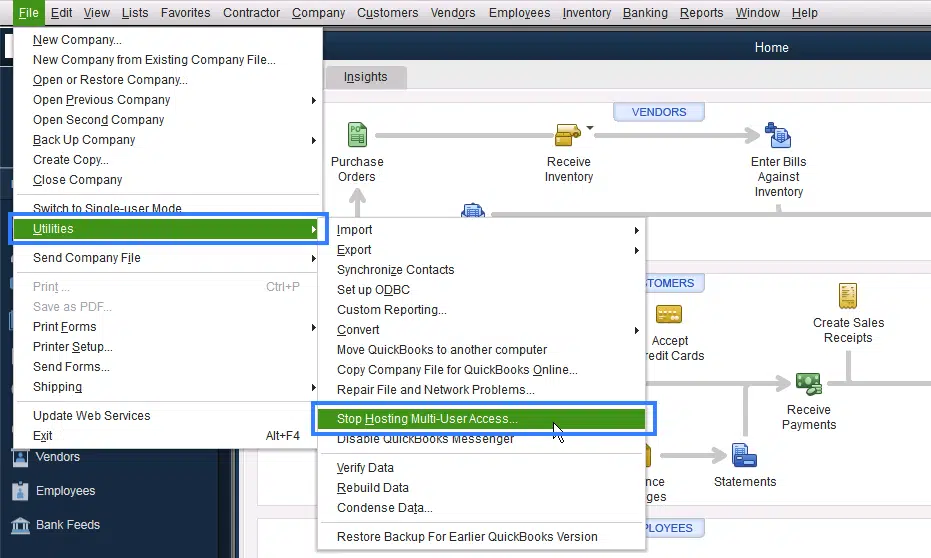

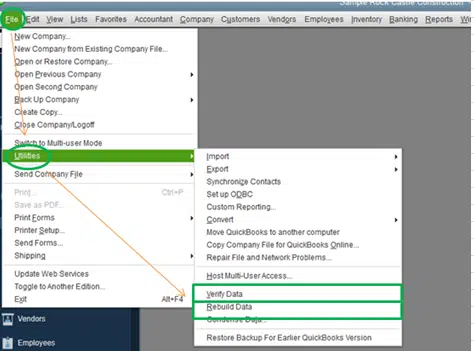

Hit a click on File menu.

Go to Utilities option.

Now hover over the Stop hosting multi-user access option.

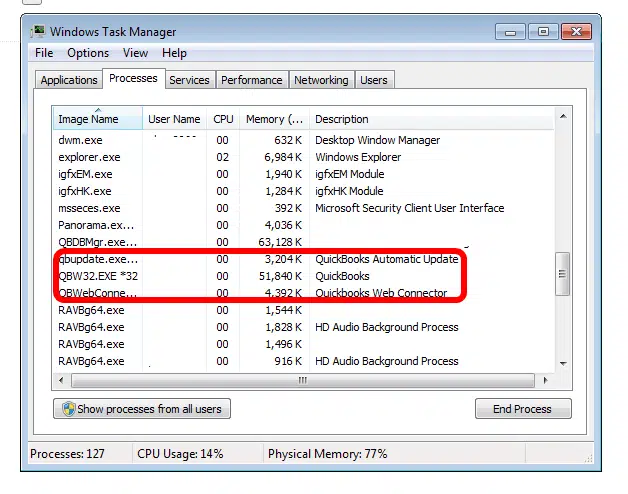

Solution 7: Close all QuickBooks processes

If none of the methods above helped you in rectifying the error 6138 1005 in QuickBooks, you probably need to turn down all QuickBooks background processes.

To begin with, sign in to the server computer using administrator credentials.

After that press the Ctrl + Shift + Esc keys together to open the Task Manager.

Now head to the Users tab.

Then look for all QB related processes running in the background.

After that hit a right-click on each QuickBooks process one by one and select the End Task/ End Process option.

Once all the QuickBooks processes are closed successfully, reopen QuickBooks desktop.

Then try opening the company file again in Multi-User Mode.

Conclusion!

Fixing QuickBooks error code 6138 1005 might seem a bit challenging for users, but the solutions discussed above are usually enough to get the issue resolved successfully. We hope that this guide has helped you to understand the causes behind the error along with the most effective troubleshooting methods to eliminate it. However, there are situations when you fail to fix the error and experience the same issue even after performing all the solutions carefully, then in that case technical guidance might be required. In such a scenario, feel free to connect with our support professionals by dialing i.e., 1-800-761-1787 and get immediate assistance for resolving all your accounting related issues.

Are you getting error codes or error messages in your QuickBooks? Well, most of these errors are related to the payroll in QuickBooks, due to which employees face difficulties in creating payroll invoices. Today in this segment, we will learn about one such common error i.e. QuickBooks error code 20102 which is usually seen by the users when your company file is unable to connect to the Intuit payroll service. This error often indicates a missing or incorrect employer identification number (EIN), a mismatch between the payroll subscription and the company file, or incomplete payroll setup.

Possible causes behind QuickBooks Payroll error 20102

There are many reasons by which QuickBooks payroll error 20102 trigger, which are follows:

Sometimes incorrect network settings causes QuickBooks to unable to access the Internet which leads to such error.

An unstable or weak Internet connection may prevent QuickBooks from downloading updates.

Security apps or Windows firewall may prevent QuickBooks from connecting to Intuit's servers.

You may also face problems if QB-related files are deleted mistakenly.

What are the Solutions to resolve the QuickBooks Error 20102?

If you are facing the QuickBooks Error 20102 then you need to apply the below solutions to fix it.

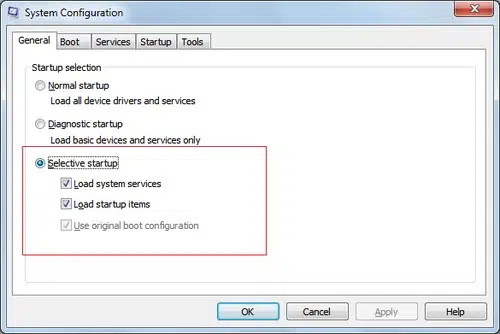

Solution 1: Update QuickBooks in selective startup mode

At first, press Windows + R keys on your keyboard to open the Run window.

In the searching tab, type Msconfig and click on OK.

After that System Configuration window will appear. Click on the General tab.

Select Selective startup and check mark on Load system services.

Now go to the Services tab and click on Hide all Microsoft services..

Then click on Disable All, then uncheck the Hide all Microsoft services checkbox.

Scroll down the list and make sure the Windows Installer box is checked. If not, check it.

Lastly hit a click on OK, then restart your computer.

Solution 2: Repairing registry entries

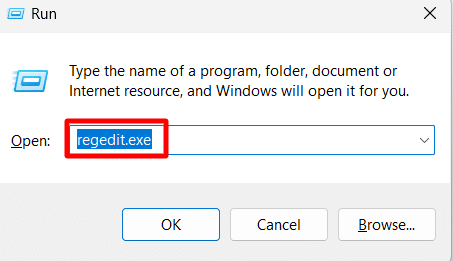

To repair registry entries first you need to restart your PC.

After that hit the Windows button from your keyboard.

You need to select Command prompt and press Ctrl+ Shit+ Enter keys.

Next hit to Yes tab.

After this a black box appear on screen.

Now type the Regedit in the run command window.

Check and select all the keys related to this QuickBooks error.

Now select the File tab then Export.

Safe the file where you want to make it secure.

Now, you need to go to the folder and give the folder a new title list.

Once done click on OK button.

After all you will find the QuickBooks backup file named reg.extension.

Solution 3: Confirm payroll services are active

Error 20102 can appear if payroll services are not activated or not linked properly.

At first, open your QuickBooks desktop.

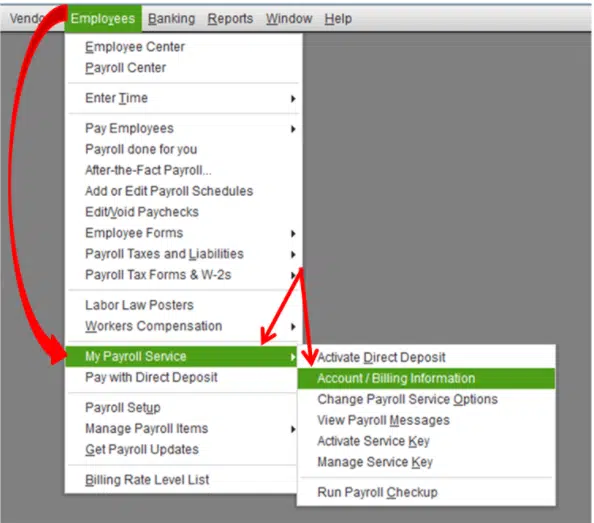

After that go to Employees tab

Select My Payroll Service and click on Account/Billing Information.

When you select File Doctor a drop-down menu will come up and you will have to select your company name. Or the name that you are using and that you want to fix at this time.

This will open the folder and you need to select the file you want and then press the "OK" button from the list.

Now, open your admin account by using your password to log in and then finally click on OK.

Solution 6: Check firewall and antivirus settings

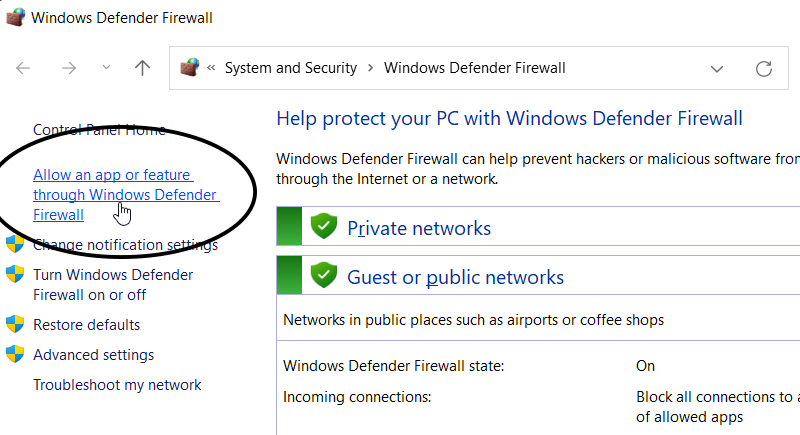

Start with pressing the Window + S keys to open the search box.

After that type "Firewall" in the search bar and select Windows Defender Firewall from the list.

Now on Windows Defender Firewall, you need to click on Allow app or feature.

Find out the QuickBooks file which is like (qbw.exe, qbupdate.exe, etc.) from the list.

Now make sure that both Private and Public checkboxes are ticked.

If you are using any 3rd party antivirus software then open its settings and add QuickBooks to the list of Exceptions.

Lastly, click on Save button and restart QuickBooks to check if the update is successful.

Conclusion

Did you find the above solutions a bit helpful in fixing the QuickBooks error code 20102? If not, then you can simply connect with our QuickBooks error support team and let our experts help you fix the error on your behalf.

FAQ's

What is QuickBooks error 20102?

Error 20102 pops up when your Employer Identification Number (EIN) is already in use or linked to another payroll account, stopping direct deposit payroll setup.

Does security software can causes QB error 20102?

Yes, sometimes firewall issues or antivirus settings can triggers such an errors by blocking communication with QuickBooks servers.

What are signs and symptoms of error 20102 in QuickBooks?

You will see repeated error messages, app crashes, or trouble with payroll and direct deposit features.

If you are a QuickBooks user from a long time, then you might be aware that this software encounters technical glitches sometimes, due to multiple reasons. These errors can be in form of numeric error codes or error messages. Today with the help of this blog post, we are going to discuss about one of the common error i.e., QuickBooks unrecoverable error while exporting to Excel (a specific error code). This error usually appears when a user try to export reports, transactions or lists from QuickBooks desktop to Microsoft Excel.

It is a critical QuickBooks desktop issue that forces the program to close unexpectedly. Also, sometimes, this error causing significant trouble for many users, so we recommend to fix this error as soon as possible. If you are getting such an error, then you are not alone, this error is a common pain point and usually occurs due to compatibility issues, outdated software or if there is some problem with Windows settings. In order to troubleshoot this unrecoverable error, keep reading this post until the end.

What Causes QuickBooks Unrecoverable Error While Exporting to Excel?

There can be several reasons behind the occurrence of this issue, Few are as:

If there is any damaged company file data.

Incompatible Microsoft Office version can also be a reason behind to such issues.

If you are using outdated QuickBooks desktop version.

In case of corrupted QuickBooks components.

How to Resolve Unrecoverable Error in QuickBooks While Exporting to Excel?

You need to follow each method in a proper sequence to troubleshoot the unrecoverable error in QuickBooks while exporting to excel and if any procedure doesn't work out, make a jump to the next method.

Solution 1: Update QuickBooks to the latest version

It is highly recommended to ensure that the QuickBooks desktop is updated to the latest release. This will fix a large number of error codes, including the QuickBooks unrecoverable error.

Open QuickBooks and run with admin rights.

Then hit on Ctrl key while double-clicking the QuickBooks icon. This will open No Company Open window on your screen.

Finally copy the data from the QBTest folder and paste it into the QuickBooks company file folder.

Solution 4: Adjust User Account Control (UAC) Settings

Press Windows + R keys together to open Run window.

After that type Control Panel and click on it.

In the next step, select the User Accounts.

Then select User Accounts (Classic View).

Once done with that, select Change user account control settings.

Note: It should be noted that, if you will get a prompt by UAC on your screen, then hit on Yes.

Now move the slider to Never Notify and select OK to turn OFF the User Account Control.

Also set to Always Notify option to turn ON the User Account Control.

Last step is to restart your system.

Final Words.!

As you reach the end of this segment, we expect you to be able to fix unrecoverable error in QuickBooks desktop while exporting to excel by using the above provided solution steps. In case the issue still persists, you can seek assistance from our technical experts via our toll-free customer support number, and let our QuickBooks desktop support team help you with your queries immediately. Help is available 24x7 through Live chat and email support.

FAQ's

Why QuickBooks unrecoverable error occurs at the time of exporting to Excel?

Some of the primary reasons for unrecoverable errors when exporting from QuickBooks to Excel include: 1. If your QuickBooks desktop or MS Excel is Outdated, it can lead to such an error. 2. There is any compatibility issues between QuickBooks and Microsoft Office. 3. Another cause can be if there is damaged or corrupt QuickBooks installation. 4. Incorrect User Account Control (UAC) settings.

Can repairing QuickBooks fix the Unrecoverable Error?

Yes. Running a QuickBooks repair from Control Panel can fix damaged program files that often trigger unrecoverable errors during export to Excel.

What should I do if the error still persists after trying all fixes?

If the problem continues even after applying all troubleshooting methods, the issue might be related to severely damaged QuickBooks or Windows components. In such cases, it’s best to get professional help.

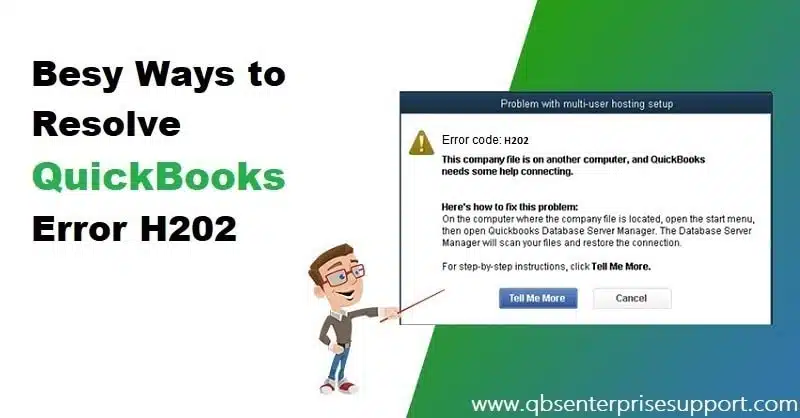

QuickBooks unrecoverable error when opening a company file on a workstation usually seen in multi-user environments when a workstation fails to access the company file stored on the server. When this error encounters, QuickBooks may crash or display an unrecoverable error message. Every error code is unique and users should note down the error code before going]g to any troubleshooting.

You need to carry out the fixation steps discussed below if you are trying to open a company file over the network through a workstation and suddenly encounter an unrecoverable error. Such a scenario might occurs, if the QBCF monitor service is running on a workstation, especially the one that is not hosting the company file. If you are also getting this error, then this guide will surely assist you. Keep reading further!

Points to remember:

Ascertain that the QuickBooks desktop is updated before performing the steps ahead.

If you are running QuickBooks on a multi-user mode and have a dedicated server or machine for storage of your company file, then affirm that the hosting is turned on in your server or main computer.

The preventive measure that can be followed here is to ascertain that the hosting is turned off in all workstations except the server.

What Causes QuickBooks Unrecoverable Error on a Workstation?

There can be various reasons behind to encountering the QuickBooks unrecoverable error. Few are as given below:

In case of incorrect hosting setup in multi-user mode.

If there is damaged QuickBooks workstation components.

Damaged or corrupted company file or program files.

If there are some kind of conflictions with system settings or services.

If firewall or antivirus are blocking the QuickBooks access, it can lead to unrecoverable error.

Sometimes this error might also occur after the Windows updates.

Insufficient folder permissions can be another cause.

Steps to Fix Unrecoverable Error in QuickBooks when opening a company file on a workstation

Checkout these solutions to fix QuickBooks unrecoverable error when opening a company file on a workstation.

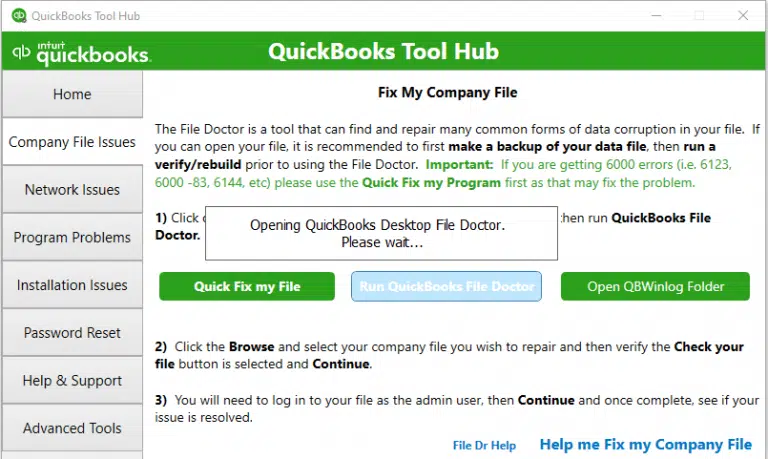

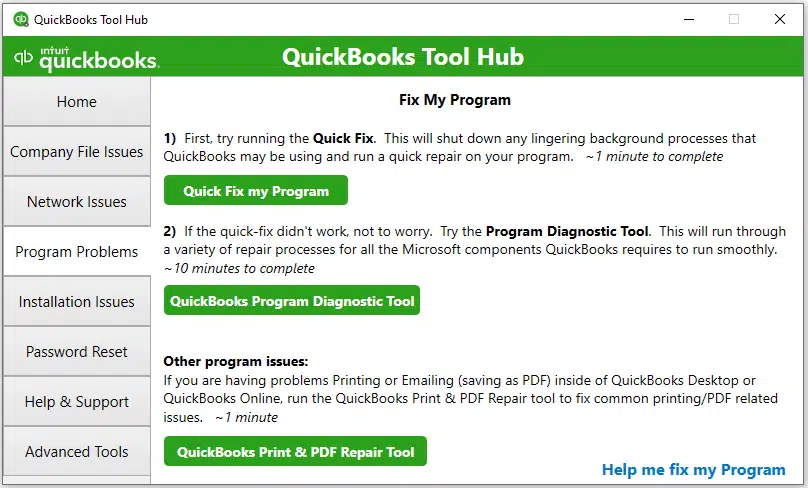

Solution 1: Download QuickBooks Tools Hub and run Quick Fix my Program

Step 1: Download and install QuickBooks Tool hub

The QuickBooks tool hub is usually used for getting rid of various annoying errors. It is highly recommended to use Tool hub program on Windows 10, 64-bit.

Save the file where it can be easily accessed. It should be noted that, if you have already installed tool hub, then you can look for the version and then select the Home tab. It will display on the bottom right or you can select the about to view the version.

Next step is to open the file which was downloaded (QuickBooksToolHub.exe)

After that carry out the on-screen set of instructions and then Install and agree to the terms and conditions.

Once the installation finishes, double click the Icon on the Windows desktop to open the tool hub.

Step 2: Run quick fix my program from the tool hub

The Quick fix my program will shut down any of the open background processes that are been used by the QuickBooks software. This will run a quick repair on the program.

Once the tool hub opens up, go to the Program problems from the left side options.

After that choose Quick fix my program.

And then start QuickBooks desktop and then open the data file.

Step 3: Disable the QBCF Monitor Service (for Network Files)

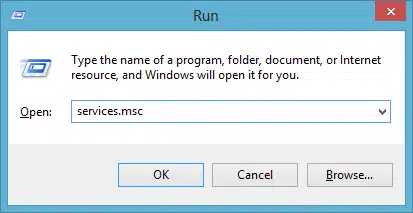

Press the Windows + R keys for opening the Run window.

Then type Services.msc and opt for the OK tab.

Head to the list and double click on QBCFMonitorService for opening the Properties tab.

Now set Startup type as Disabled.

End the process with selecting Apply and OK tabs respectively.

Solution 2: Troubleshooting of QuickBooks Desktop

Step 1: Repair QuickBooks Desktop

Access the Reboot.exe in order to re-register QB objects in the Windows.

After that manually Repair the installed Microsoft.net framework.

We hope that the above provided steps has assisted you to troubleshoot the QuickBooks unrecoverable error when opening a company file on your workstation. However, we also understand that for every user it is not comfortable to follow these technical troubleshooting methods. If you still encounter the error or you need any further assistance, don’t hesitate to connect with our QuickBooks error support team for immediate technical assistance.

QuickBooks error code 1749 generally occurs due to problems related to software’s internal files or issues with the other program running on background or may be issue popped-up during an update process. This error might also be triggered by corruption in the company files or cause error in the system registry. According to experts, this error can also bothered you while updating the software or performing certain processes. It is a common error, and can interrupt your workflow for time to time. This error may corrupt your company file or Windows registry. Thus, it is important to rectify this error as soon as possible.

If you are getting such an error on your QuickBooks, then don't worry, you have landed into right place. In this segment we will elaborate what is this error and why it arises and how you can solve it easily.

What are the causes of QuickBooks error 1749?

Below are some possible reasons due to which error code 1749 in QuickBooks desktop may encounter in your system:

QuickBooks is not downloaded or installed properly on the system.

Corrupted Window Registry related to this error can be another reason.

Error code 1749 may also occurs if system is affected by some Viruses or Malware.

Antivirus installed in the system may cause problems to run QuickBooks works efficiently.

If some of the files in the Windows registry may be deleted accidentally.

A poor internet connection can be also a reason.

Updated Fixation Methods for QuickBooks Error 1749

Below are some DIY methods in order to resolve the QuickBooks error 1749. Apply every step one-by-one and reboot your system.

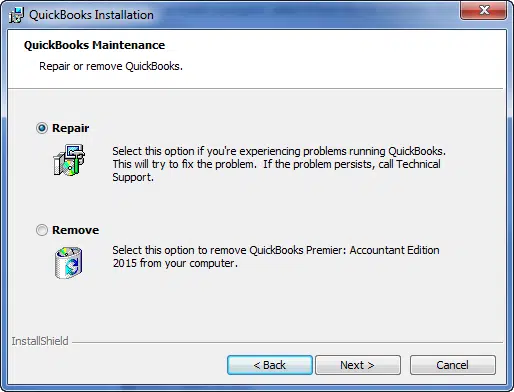

Solution 1: Repair QuickBooks desktop

Click on Start button and type Control Panel in the search bar and select to open.

After that locate Add or Remove Programs.

In the list of programs you can look out for the QuickBooks.

After that right click on the QuickBooks icon and select Repair option.

Wait till your system is in repairing process.

Once done, restart your computer.

Now open your QuickBooks and check the error is resolved.

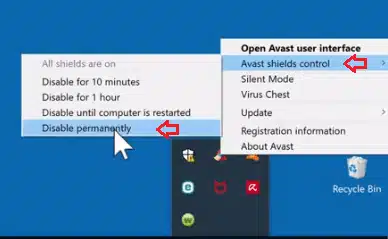

Solution 2: Run QuickBooks in safe mode

Find the antivirus software icon in the taskbar.

After that hit a right click on the Antivirus icon.

From the menu, go to the Options tab.

Then select Disable option from the dropdown menu.

Now click on OK to save the changes and restart your system.

Lastly, open QuickBooks on your system and launch QuickBooks in safe mode.

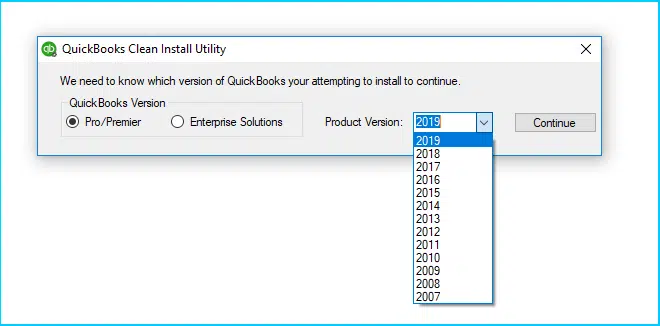

Solution 3: Download and install the QuickBooks Tool Hub

QuickBooks tool hub program is set of different-different tools that can fix many QuickBooks related errors. Follow the below given steps in order to resolve this error.

Close all the applications running on your system.

From the official website download QuickBooks tool hub and save the file with named QuickBooksToolHub.exe.

The tool will automatically rename the installation folders which is associated with QuickBooks.

If the clean install tool encounters any problems while renaming folders, then you may need to rename the files manually. Following are the common folders to rename:

The last step is to reinstall QuickBooks desktop on your system using license and product information. Don't forget to activate your QuickBooks desktop.

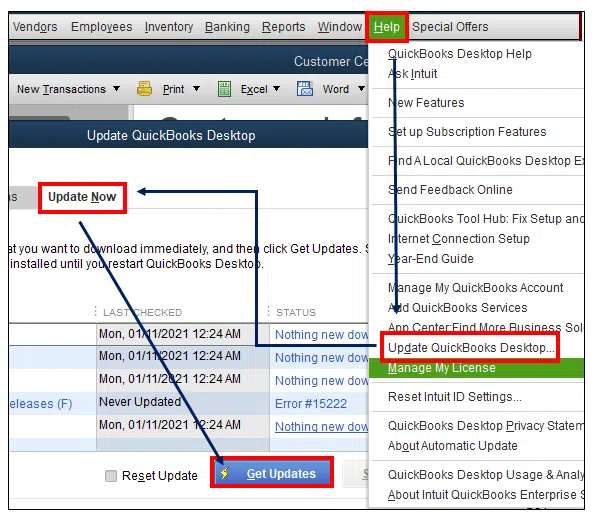

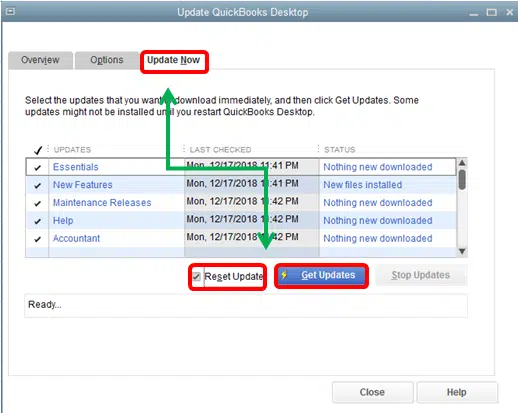

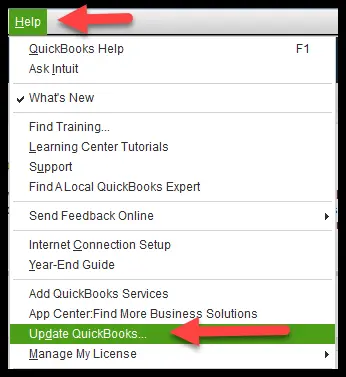

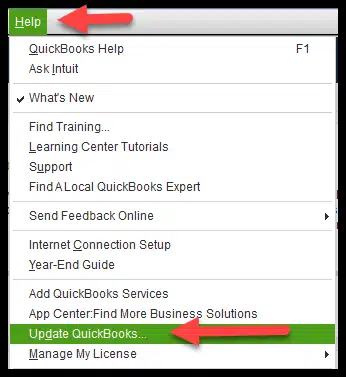

Navigate to the Help menu and select Update QuickBooks desktop.

In the update QuickBooks window select Update now.

Now tap on the check box for Reset update to remove previously downloaded updates.

Then click on Get updates.

Once the update process finish, restart your QuickBooks and check if the error continues or resolved.

Conclusion

Hope the above provided solutions helped you to rectify the QuickBooks error code 1749 by your own. In case the issue still persists on your system, then don't waste much time in applying the steps again and again. You need to speak to our 24/7 QuickBooks error support experts for the best in the industry services. Our U.S based helpline number is 1-800-761-1787. Our experts are available round the clock to serve you industries best support services via Live chat, toll-free and email support.

FAQ's

How do I prevent Error 1749 from happening again?

To reduce the risk of this error happen again in future, you need to keep your QuickBooks and Windows OS updated and regularly back up your data.

What are the Symptoms of QuickBooks Error code 1749

1. A continuous error message start popping up on the screen that QuickBooks encountered a problem and needs to be restart. 2. QuickBooks desktop crashes suddenly while working on the 3. System may be freeze or works too slow while operating the software.

How do I know if I am experiencing Error 1749?

You will get a pop-up message with the error code while working with QuickBooks or your program may crash or slowdown.